破局存量,红海掘金:山东分公司燃油二手车车险转型实战复盘

Breaking Through the Existing Market and Finding Growth in a Red Ocean: A Practical Review of Shandong Branch’s Transformation in Fuel-Powered Used-Car Auto Insurance

引言

面对二手车车险道德风险高、风险因子复杂、渠道把控难等行业痛点,以及监管趋严、业务结构优化的迫切需求,山东分公司于2024年率先锚定燃油二手车车险赛道,确立“低费高价”的核心战略。通过深度市场调研、差异化区域策略及全流程风控体系建设,实现签单保费同比增长59%,全司业务占比提升至63%,成本可控,探索出一套可复制、可落地的存量业务转型方法论。

机构转型名片

– 项目名称:燃油二手车车险转型项目

– 牵头机构:山东分公司

– 转型关键词:存量破局、风险精控、低费高价、渠道深耕

– 核心数据亮点:

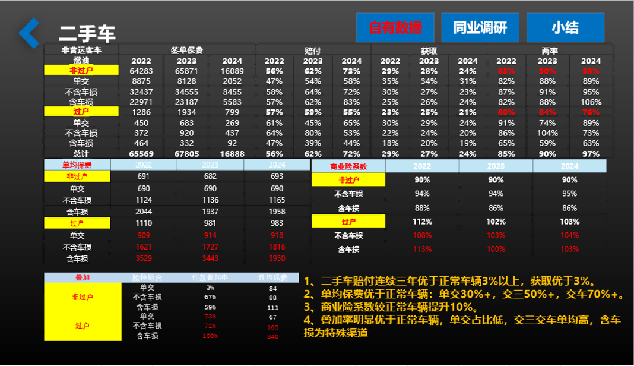

- 规模增长:2025年机构二手车签单保费同比增速59%。

- 结构贡献:二手车业务全司占比高达63%,较2024年提升12个百分点。

- 经营质效:保单成本实现盈利,实现规模与效益双优。

对话机构一把手:山东分公司总经理吴波

“低费高价,不是保守,而是跳出粗放竞争、回归长期经营的主动选择。”

问题一:2024年,行业对二手车车险多是粗放拓展模式,您为何提出“低费高价”这一核心思路?

放眼2024年整体保险市场,多数主体仍在拼费用、抢份额,导致行业费用持续高位、盈利空间收窄。加之我司2023年新能源业务已出现明显亏损,且“优质优费”策略与当前高压监管态势相悖。因此,我们选择 “低费”——严控渠道费用、优化业务成本,摒弃无效费用投入,拒绝恶性价格战,将经营重心从费用比拼转向服务与风控,实现成本可控、经营可持续;“高价”——在精准承保的前提下,聚焦优质业务、提升定价充足度,筛选良性标的、提高业务品质,最终实现公司、客户、渠道三方共赢。

可以说,“低费高价”的本质是跳出粗放竞争,回归长期健康经营理念,契合总公司高质量发展的战略导向,也是基于监管形势与市场竞争压力作出的精准抉择。

问题二:当总部提出燃油二手车可作为发展方向时,山东分公司是如何快速完成从“方向参考”到“本地落地策略(单交/交三)”的转化的?

关键在于快速响应与本地化落地。

首先,全员下沉开展调研。分公司销管部、车险部联动各地市机构车险团队,对山东本地二手车市场体量、车源结构、车主消费习惯、渠道合作模式及同业成本结构等进行全方位摸底。

其次,精准锁定主攻产品与渠道策略。鉴于二手车业务道德风险相对较高,车险部在充分考量理赔队伍配置的基础上,精准梳理出以燃油“单交+交三”为主攻方向,明确核心业务场景与产品需求。优化承保规则,针对燃油二手车风险特征合理设定承保条件,在严控风险的前提下提升报价量与成交率。

最后,快速启动机构试点与标准化落地。精准对接本地二手车交易市场、头部二手车商、汽车修理厂、大型中介等核心渠道,制定适配山东市场的承保规则与渠道政策,选取济南、潍坊、临沂、德州、聊城等机构先行试点;同步召开全省专项会议宣导,明确业务目标、操作规范与考核导向,确保策略执行不走样。

问题三:项目启动时,二手车市场鱼龙混杂且道德风险高发,您是如何敲定“先试点、严管控”的推进节奏,平衡业务拓展与风险防控的?

二手车市场主体繁杂、车辆状况参差不齐,骗保、虚假投保等道德风险突出,是行业公认的共性难题。盲目全面铺开,极易引发大规模风险亏损,背离了高质量发展的初衷。为此,在充分调研、反复研判和审慎决策的基础上,我们最终确立了“先试点、严管控”的推进节奏,核心是守住风险底线,实现业务拓展与风险防控的动态平衡。

试点先行,坚持“小范围试水、精细化打磨、可复制推广”。优先选择规模基础扎实、风控队伍完善的重点地市开展试点,快速验证策略可行性并及时优化;严格筛选业务标的,明确试点范围、承保限额与客户准入标准,不盲目追求规模。通过小范围试点打磨风控流程、积累风险处置经验,成熟后再稳步向全省复制推广,从源头降低大规模业务风险。

闭环风控,构建全流程风险管控体系。依托公司风险定价及外部风控模型,对投保信息、车辆车况、历史理赔数据进行实时核验,强化承保核保管控,堵住虚假投保漏洞;建立专项风控排查小组,对二手车车险理赔案件从严审核,坚决打击骗保等道德风险;建立风险预警机制,实时监控业务数据,一旦发现隐患,第一时间叫停整改,确保风险可控。

我们始终认为,二手车车险业务拓展必须风控先行。“先试点、严管控”的节奏,既保障了业务稳步有序推进,又牢牢守住了风险底线,确保二手车保险业务在合规稳健的前提下实现可持续、高质量发展。

对话项目负责人:山东分公司副总经理胡炜

“因地制宜,用数据说话——从零开始,我们趟出了一条可监控、可调控、可复制的路。”

问题一:接到项目时,总部仅给出燃油二手车的发展方向,无现成落地方案,且内部缺乏实操经验。您最想分享的核心心得是什么?

第一,把握政策与市场红利,理性研判业务风险。

依托国家新能源战略转型、汽车以旧换新国补及省补政策,二手车市场销量迎来高速增长,夫妻过户、亲属过户等业务批量涌现。从实际风控来看,这类合规过户业务的风险并未出现明显抬升;但二手车整体风险显著高于普通非过户车辆,且潜藏不少道德风险,对管理能力和专业水平要求极高,也因此限制了市场入局主体的数量。基于此,我们确立了核心原则:不拉高渠道费用,不扰乱区域市场,依托自身成熟的管理体系、广泛的渠道触达能力和灵活的销售节奏,稳中求进布局业务,不走激进路线。

第二,因地制宜差异化经营,结合地市机构特色精准破局。

各地二手车市场形态差异显著,不能以一套规则通用全省。以临沂为例:2024年放开鲁W双牌照后,大量吉祥号、靓号号牌集中释放,市民争相抢号,由此催生旧车占号、夫妻过户、亲子过户、个人转企业乃至僵尸车过户、过户至未成年人等多样化场景。这类车辆实际风险并未明显增加,但保费充足度提升超过40%。临沂中支精准把握这一窗口期,及时优化核保规则,对优质良性业务适度放宽年龄、车龄等限制,稳稳吃下市场红利。

再如济南拥有全国头部二手车平台瓜子二手车,潍坊有全省领先的中高端二手车平台蚂蚁好车——每个地市都有自身的资源禀赋与市场标签。我们坚持“一机构一策略”,走多元化、差异化的发展路径,以本地市场特点为根基开展业务。

第三,沉淀标准化项目管理体系,以数据闭环驱动良性发展。

在从零推进二手车项目的过程中,我们同步构建了一套覆盖机构、渠道、项目全维度的成熟管理体系。依托自有系统优势,建立起“报价量监控—核保通过率动态调整—业务成交率提升”的数据化闭环管控机制,以真实数据为指引,反向引导地市机构优化经营节奏、调整核保尺度、提升转化效能,让二手车业务从摸索试水演进为可监控、可调控、可复制的标准化经营模式。

问题二:为规避道德风险,团队亲赴山东各地二手车市场进行多轮专项调研。哪些场景令您印象最深?有没有哪个瞬间打破了团队原有的判断?这些“意外”最终如何转化为本地专属风控举措?

这次调研遍及山东各地二手车交易市场与集散地。最深的体会是:眼见为实才能颠覆认知,实地调研才能突破经验惯性。尤其是车险作假、套路过户、刻意包装车况这几类场景,彻底刷新了我们原有的常规风控逻辑,也倒逼我们重新搭建本地化的风控规则体系。

场景一:集中批量过户的“套路车集群”乱象。很多地市二手车市场周边,聚集着大量代办过户、代办号牌、代办车险的中介工作室。操作模式并非单车零散交易,而是成批打包推进——夫妻过户、亲子过户、个人转企业过户,乃至批量过户至未成年人或空壳企业名下,一应俱全。表面上看是正常的二手车流转,实则是车商借助过户规则进行车况洗白与风险隔离,将事故车、调表车、泡水车通过多次过户逐步淡化历史痕迹,再流向终端客户。整套操作链条成熟、分工明确,从常规车辆档案中几乎难以发现破绽。

场景二:车险专业作假团队产业化运作,隐蔽性极强。这是调研中最触目惊心的发现:市场里存在专业化的车险黑色产业链作假团队,分工精密、流程规范——有人专门收购问题车,有人负责篡改车况里程,有人伪造维修记录,有人对接渠道完成投保,还有人专职策划后期虚假理赔。这些团队对保险公司常规核保审核要点了如指掌,能精准规避系统风控节点,利用二手车信息不对称与过户信息割裂的漏洞,将问题车包装成普通个人代步车投保,从中牟取保费差价与理赔获利。其作案手法高度本地化,常规教科书式的风控标准几乎难以奏效。

基于这些来自一线的认知颠覆,我们彻底放弃通用化、模板化的风控逻辑,针对性出台了山东本地专属风控举措:

一是实行地市差异化风控尺度。结合临沂、济南、潍坊等各地市场特点,不搞全省一刀切,针对双牌照城市、大型二手车集散地、中高端二手车集群等不同区域,定制专属核保政策与风控强度,做到“一地一风控、一类场景一规则”。

二是搭建内部风险案例共享库。将调研中发现的作假套路、典型风险场景与识别特征全部整理入库,并针对过户、投保时间节点创建“A、A1、B、B1”四维风控标准;同步对机构和渠道一线人员开展专项培训,从“只看数据”转变为“懂市场、识套路、辨人为包装”,全面提升对道德风险与车险作假行为的识别能力。

问题三:项目推进中,需要定价核保、承保、理赔、销管等多部门协同,在落实“低费高价”和风险管控的过程中,如何打破条线壁垒,确保各部门执行标准统一、动作高效配合?

我们以“低费高价+风险管控”为统一目标,建立统一规则、统一流程,将定价核保、承保、理赔、销管从“各管一摊”整合为“一条链路闭环”,从机制层面打破条线壁垒。

一是成立二手车保险专项跨部门工作组。由销售管理部牵头,定价核保、承保审核、理赔风控、销售管理、渠道管理、合规风控等部门整体配合,形成固定例会机制,建立全新板块业务发展月报监控。

二是形成统一的二手车保险执行策略。以分公司统一承保准入为基准、机构特色化核保调整为辅助,结合风控联动闭环,实现理赔数据反向赋能核保定价、动态迭代执行标准:

- 理赔端建立二手车风险案例库,涵盖事故高发车型、高频骗保渠道、营转非高风险车辆、维修虚高案例,定期同步核保与销管部门;

- 定价核保根据理赔风险数据动态调整费率系数与准入门槛,同步更新执行手册;销管同步调整渠道展业方向;

- 销管对高风险渠道、高风险业务实行限流或暂停准入,从源头管控业务量与风险,确保“低费高价”落地不盲目冲量。

内部研讨

2024年半年会第一次分享二手车项目

2024年年会确立二手车项目目标

实地调研

机构推动

Introduction

Facing industry pain points in used-car auto insurance, such as high moral hazard, complex risk factors, and difficulty in channel control, as well as the urgent need for stricter regulatory compliance and business structure optimization, Shandong Branch took the lead in 2024 by focusing on the fuel-powered used-car auto insurance segment and establishing a core strategy of “low commission and high pricing.”

Through in-depth market research, differentiated regional strategies, and the construction of an end-to-end risk control system, the branch achieved a 59% year-on-year increase in signed premiums. Its share of the company’s used-car business rose to 63%, while costs remained under control. This has created a replicable and implementable methodology for transforming existing business.

Branch Transformation Profile

Project Name: Fuel-Powered Used-Car Motor Insurance Transformation Project

Leading branch: Shandong Branch

Transformation Keywords: Breaking through the existing market, precise risk control, low commission and high pricing, deep distribution cultivation

Core Data Highlights:

- Scale Growth: In 2025, the branch’s used-car signed premiums increased by 59% year-on-year.

- Structural Contribution: Used-car business accounted for as much as 63% of the company’s total used-car business, up 12 percentage points from 2024.

- Operating Quality: Policy costs achieved profitability, delivering both scale growth and efficiency improvement.

Interview with the Branch General Manager Mr. Wu Bo

“Low commission and high pricing is not a conservative choice. It is a proactive decision to move beyond extensive competition and return to long-term business management.”

Question 1: In 2024, most players in the industry were still expanding used-car motor insurance in an extensive manner. Why did you propose the core idea of “low commission and high pricing”?

Looking at the overall insurance market in 2024, most market players were still competing through commissions and market share, which led to persistently high industry expenses and shrinking profit margins. In addition, our company had already seen significant losses in its new energy vehicle business in 2023, while the “better quality, better commission” strategy ran counter to the current high-pressure regulatory environment.

Therefore, we chose “low commission” — strictly controlling distribution expenses, optimizing business costs, abandoning ineffective expenditure, and refusing to engage in vicious price wars. We shifted our operating focus from commission-based competition to service and risk control, thereby making costs controllable and operations sustainable.

We chose “high pricing” — under the premise of precise underwriting, focusing on high-quality business, improving pricing adequacy, selecting sound risks, and enhancing business quality. Ultimately, this creates a win-win outcome for the company, customers, and channels.

In essence, “low commission and high pricing” means moving beyond extensive competition and returning to a philosophy of long-term and healthy business management. It aligns with the head office’s strategic direction of high-quality development and is also a precise choice made in response to the regulatory environment and market competition pressures.

Question 2: When the headquarters identified fuel-powered used cars as a potential development direction, how did Shandong Branch quickly transform this from a “directional reference” into a localized implementation strategy, namely compulsory-only and compulsory-plus-third-party-liability products?

The key lay in rapid response and localized implementation.

First, all staff went down to the front line to conduct research. The branch’s Sales Management Department and Motor Insurance Department worked together with motor insurance teams across prefecture-level institutions to conduct a comprehensive review of the local used-car market in Shandong. This included market size, vehicle source structure, car owner consumption habits, distribution cooperation models, and peer company cost structures.

Second, we precisely identified the main products and distribution strategy. Given the relatively high moral hazard in used-car business, the Auto Insurance Department fully considered the configuration of the claims team and then identified fuel-powered “compulsory-only” and “compulsory plus third-party liability” products as the main focus. We clarified the core business scenarios and product demand, optimized underwriting rules, and reasonably set underwriting conditions based on the risk characteristics of fuel-powered used cars. This improved quotation volume and conversion rates while keeping risks under strict control.

Finally, we rapidly launched institutional pilots and standardized implementation. We precisely connected with core distributions such as local used-car trading markets, leading used-car dealers, motor repair shops, and major intermediaries. We formulated underwriting rules and channel policies adapted to the Shandong market, and selected branches in Jinan, Weifang, Linyi, Dezhou, Liaocheng, and other areas for initial pilots. At the same time, we held a province-wide special meeting to communicate the strategy, clarify business objectives, operating standards, and assessment orientation, ensuring that implementation did not deviate from the intended direction.

Question 3: At the start of the project, the used-car market was highly mixed and moral hazard was frequent. How did you decide on the pace of “pilot first, strict control,” and how did you balance business expansion with risk prevention?

The used-car market involves complex market participants and vehicles of uneven quality. Moral hazards such as insurance fraud and false applications are prominent, which is a common industry challenge. If we had expanded blindly across the board, it would have been very easy to trigger large-scale risk losses, contradicting the original intention of high-quality development.

Therefore, based on sufficient research, repeated analysis, and prudent decision-making, we ultimately established a pace of “pilot first, strict control.” The core was to hold the risk bottom line and achieve a dynamic balance between business expansion and risk prevention.

Pilot first, adhering to “small-scale testing, refined improvement, and replicable promotion.” We prioritized key cities with a solid business foundation and mature risk control teams for pilot implementation. This allowed us to quickly verify the feasibility of the strategy and optimize it in time. We strictly screened business targets, clarified pilot scope, underwriting limits, and customer access standards, and did not blindly pursue scale. Through small-scale pilots, we refined risk control processes and accumulated risk handling experience before steadily replicating the model across the province, thereby reducing large-scale business risk from the source.

Closed-loop risk control, building an end-to-end risk management system. Relying on the company’s risk pricing and external risk control models, we conducted real-time verification of application information, vehicle condition, and historical claims data. We strengthened underwriting and approval controls to close loopholes in false insurance applications. We established a special risk control investigation team to strictly review claims cases involving used-car motor insurance and resolutely crack down on moral hazards such as insurance fraud. We also established a risk early-warning mechanism to monitor business data in real time. Once hidden risks were identified, rectification was immediately initiated to ensure that risks remained controllable.

We have always believed that risk control must come first in the development of used-car motor insurance. The pace of “pilot first, strict control” not only ensured steady and orderly business progress, but also firmly held the risk bottom line, enabling used-car insurance business to achieve sustainable and high-quality development under compliant and prudent conditions.

Interview with the Project Lead Mr. Hu Wei, Deputy General Manager of Shandong Branch

“Adapt to local conditions and let data speak. Starting from zero, we carved out a path that is monitorable, adjustable, and replicable.”

Question 1: When you received the project, the headquarters had only provided the development direction of fuel-powered used cars. There was no ready-made implementation plan, and the organization lacked internal operating experience. What is the most important lesson you would like to share?

First, seize policy and market opportunities while rationally assessing business risks.

Driven by the national strategy for new energy transformation, as well as national and provincial subsidies for vehicle trade-ins, the used-car market saw rapid growth in sales. Scenarios such as transfers between spouses and relatives emerged in large volumes. From an actual risk control perspective, these compliant transfer transactions did not show any obvious increase in risk. However, the overall risk of used cars is significantly higher than that of ordinary non-transferred vehicles, and there are many hidden moral hazards. This places extremely high demands on management capability and professional expertise, which also limits the number of market participants.

Based on this, we established a core principle: do not raise distribution commissions, do not disrupt the regional market, and rely on our mature management system, broad distribution reach, and flexible sales rhythm to steadily develop the business. We chose not to pursue an aggressive route.

Second, adopt differentiated operations according to local conditions and break through precisely based on the characteristics of each prefecture-level institution.

Used-car markets vary significantly from place to place, so one set of rules cannot be applied across the whole province. Take Linyi as an example. After the opening of the Lu W dual-license-plate policy in 2024, a large number of lucky and attractive plate numbers were released, prompting residents to compete for them. This created diverse scenarios such as using old cars to reserve plate numbers, transfers between spouses, transfers between parents and children, transfers from individuals to enterprises, and even transfers of dormant vehicles or transfers to minors. The actual risk of such vehicles did not increase significantly, but premium adequacy rose by more than 40%. Linyi Central Sub-branch accurately captured this window of opportunity, promptly optimized underwriting rules, and moderately relaxed restrictions on age and vehicle age for high-quality, sound business, thereby steadily capturing the market opportunity.

Another example is Jinan, which has Guazi Used Cars, one of the country’s leading used-car platforms. Weifang has Ant Good Car, a leading mid-to-high-end used-car platform in the province. Each prefecture-level market has its own resource endowment and market characteristics. We adhered to the principle of “one strategy for one branch” and pursued a diversified and differentiated development path rooted in local market characteristics.

Third, establish a standardized project management system and drive sound development through a data-based closed loop.

In the process of promoting the used-car project from scratch, we simultaneously built a mature management system covering branches, distributions, and projects across all dimensions. Relying on the advantages of our own systems, we established a data-based closed-loop management mechanism of “quotation volume monitoring — dynamic adjustment of underwriting approval rate — improvement of business conversion rate.” Guided by real data, we helped prefecture-level institutions optimize their operating rhythm, adjust underwriting standards, and improve conversion efficiency. This enabled used-car business to evolve from exploratory testing into a standardized operating model that is monitorable, adjustable, and replicable.

Question 2: To avoid moral hazard, the team personally visited used-car markets across Shandong for multiple rounds of special research. Which scenarios left the deepest impression on you? Was there any moment that overturned the team’s original judgment? How were these “surprises” ultimately transformed into localized risk control measures?

This research covered used-car trading markets and distribution centers across Shandong. The strongest feeling was that seeing is believing. Only on-site research can overturn assumptions and break through experience-based inertia. In particular, several scenarios — motor insurance fraud, manipulated transfers, and deliberate packaging of vehicle conditions — completely refreshed our conventional risk control logic and forced us to rebuild a localized risk control rule system.

Scenario 1: The disorder of “scheme-based vehicle clusters” involving concentrated batch transfers. Around used-car markets in many cities, there are large numbers of intermediary offices that handle ownership transfers, license plates, and auto insurance. Their operating model is not scattered single-vehicle transactions, but batch-based packaged operations. Transfers between spouses, transfers between parents and children, transfers from individuals to enterprises, and even batch transfers to minors or shell companies are all available. On the surface, these appear to be normal used-car transactions. In reality, dealers use transfer rules to whitewash vehicle conditions and isolate risks. Accident vehicles, odometer-tampered vehicles, and flood-damaged vehicles are repeatedly transferred to gradually dilute historical traces before being sold to end customers. The entire operation chain is mature and clearly divided in responsibilities, making it almost impossible to detect problems from ordinary vehicle records.

Scenario 2: Professional motor insurance fraud teams operating industrially and with strong concealment. This was the most shocking discovery during the research. There are professional black-market motor insurance fraud teams in the market, with precise division of labor and standardized processes. Some people specialize in acquiring problem vehicles, some modify vehicle conditions and mileage, some forge repair records, some connect with channels to complete insurance applications, and others specialize in planning subsequent false claims. These teams are highly familiar with the routine underwriting review points of insurance companies and can accurately avoid system risk control nodes. By exploiting information asymmetry in used cars and the fragmentation of transfer information, they package problem vehicles as ordinary personal-use vehicles for insurance, thereby profiting from premium differences and claims payouts. Their methods are highly localized, and conventional textbook-style risk control standards are almost ineffective.

Based on these frontline insights that overturned our previous understanding, we completely abandoned generic and template-based risk control logic and introduced targeted risk control measures tailored specifically to Shandong.

First, we implemented differentiated risk control standards by prefecture-level market. Combining the market characteristics of Linyi, Jinan, Weifang, and other areas, we avoided a one-size-fits-all approach across the province. For different regions, such as dual-license-plate cities, large used-car distribution centers, and mid-to-high-end used-car clusters, we customized underwriting policies and risk control intensity, achieving “one local risk control strategy for one region, and one rule for one type of scenario.”

Second, we built an internal risk case-sharing database. We organized and entered into the database all fraudulent methods, typical risk scenarios, and identification features discovered during the research. We also created four-dimensional risk control standards — “A, A1, B, and B1” — based on transfer and application time points. At the same time, we provided special training for institutional and channel frontline staff, helping them shift from “only looking at data” to “understanding the market, recognizing schemes, and identifying artificial packaging.” This comprehensively improved their ability to identify moral hazard and auto insurance fraud.

Question 3: The project required collaboration among pricing and underwriting, policy issuance, claims, sales management, and other departments. In the process of implementing “low commission and high pricing” and risk control, how did you break down departmental barriers and ensure unified standards and efficient coordination across departments?

We used “low commission and high pricing plus risk control” as the unified objective and established unified rules and processes. This integrated pricing and underwriting, policy issuance review, claims risk control, sales management, distribution management, and compliance risk control into “one closed-loop chain,” breaking down departmental barriers at the mechanism level.

First, we established a special cross-departmental working group for used-car insurance. Led by the Sales Management Department, the group brought together pricing and underwriting, policy issuance review, claims risk control, sales management, distribution management, compliance risk control, and other departments. A fixed regular meeting mechanism was established, along with a new monthly business development monitoring report for this sector.

Second, we developed a unified execution strategy for used-car insurance. Based on the branch’s unified underwriting access standards, supplemented by institution-specific underwriting adjustments, and combined with a closed-loop risk control mechanism, we enabled claims data to feed back into underwriting and pricing, dynamically iterating execution standards.

- The claims side established a used-car risk case database covering accident-prone vehicle models, high-frequency fraud channels, high-risk commercial-to-non-commercial vehicles, and inflated repair cases. This information was regularly shared with underwriting and sales management departments.

- Pricing and underwriting dynamically adjusted rate factors and access thresholds based on claims risk data, and updated the execution manual accordingly. Sales management simultaneously adjusted channel business development directions.

- Sales management implemented flow restrictions or suspended access for high-risk channels and high-risk business. This controlled business volume and risk from the source, ensuring that “low commission and high pricing” was implemented without blindly pursuing volume.